What are the different types of inventory?

There are several types of inventory: perpetual inventory, annual inventory, and cycle counting. Their purpose is to verify the counted stock against the theoretical stock. Any difference between the two is referred to as inventory discrepancies.

Types of inventory: annual inventory

The annual inventory is often carried out at the end of the accounting period.

The annual inventory, also called a periodic inventory, consists of counting all items. It requires a specific procedure and can be quite complex, as it necessitates additional staff. Therefore, companies often call upon temporary workers or all employees, regardless of their role, for this purpose. Conducting the annual inventory requires a halt to production and can thus be quite costly.

All products must be counted: merchandise, raw materials, finished goods, and semi-finished goods. It is necessary to count everything belonging to the company, including off-site inventory. This refers to inventory belonging to the company but located in a different storage location. All areas must be properly identified for counting purposes.

Types of inventory: Perpetual inventory

Perpetual inventory involves counting inventory with each inflow or outflow (supplies or sales). It is quite time-consuming and is generally used by companies with small inventory levels. However, this method has the advantage of always providing up-to-date inventory data.

Types of inventory: Cycle counting

Cycle counting involves conducting inventories several times a year. During these counts, not all items are counted at the same intervals.

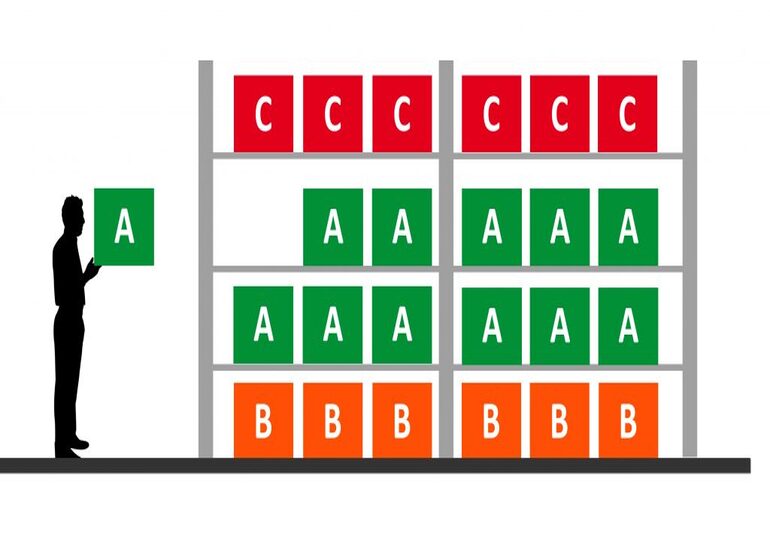

The list of items counted is based on a methodology chosen by the company. Among the methodologies, we find the ABC method: items are classified into categories A, B, or C. These categories represent the counting frequency (for example, A: once a month, B: once a quarter, C: once a year). Items are classified into these categories based on criteria chosen by the company. These criteria include, for example, the stock valuation or the value of inventory discrepancies. Items with the highest valuations or those with the largest inventory discrepancies will be in category A and will be counted most frequently.

Cycling inventory requires monitoring, often carried out by the management accountant, which allows for precise tracking of the items counted, the stock valuation, the value of inventory discrepancies, etc.

Cycling inventory represents a middle ground between perpetual inventory and annual inventory. It allows for addressing inventory discrepancies without overburdening the system.

January 25, 2026 - BY Admin

January 25, 2026 - BY Admin